Carmignac P. EM Debt: Letter from the Fund Managers

Carmignac P. EM Debt lost -1.88% in the third quarter of 2023, while its reference indicator1 was down -0.94%.

Market environment

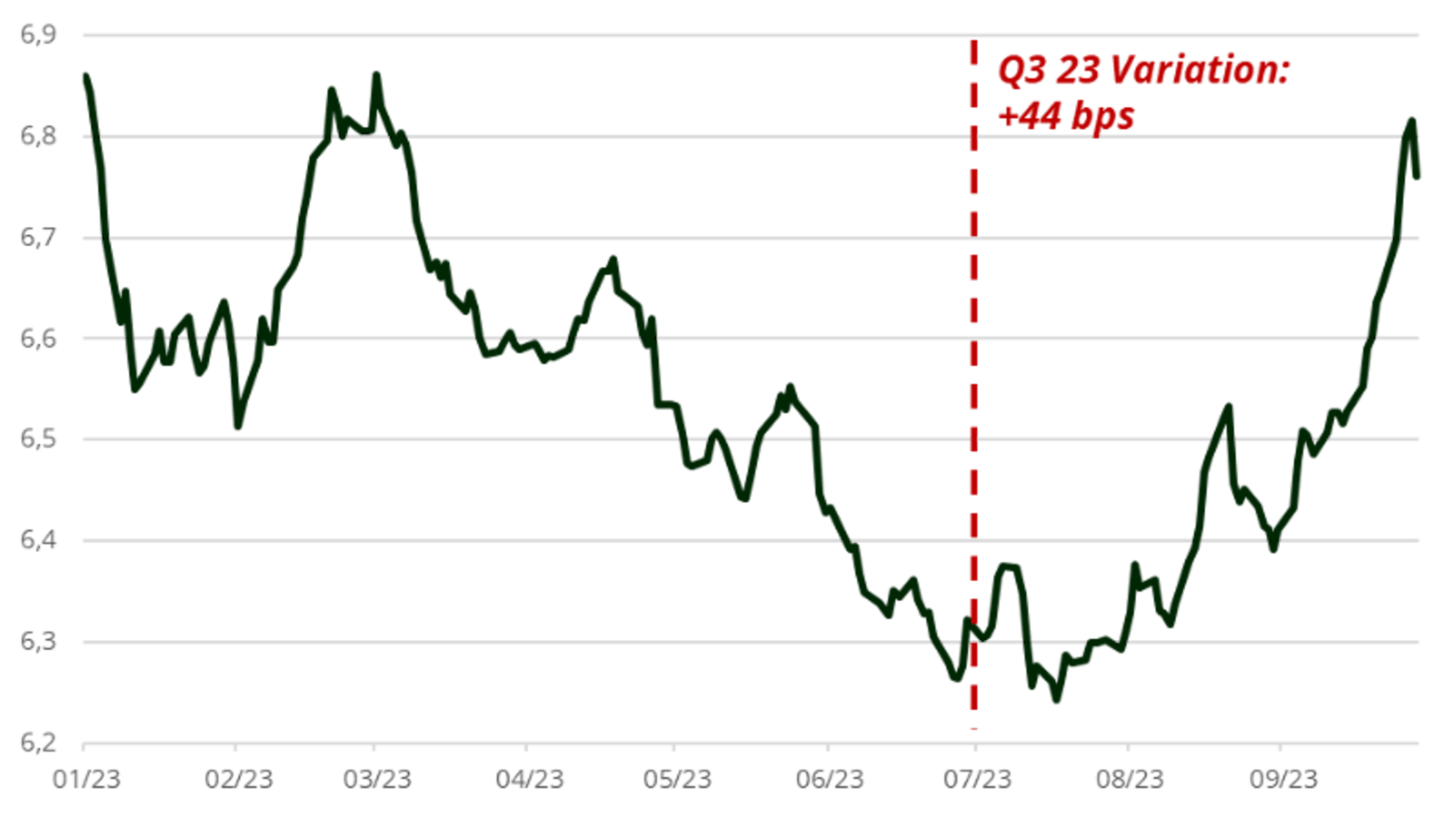

The third quarter of 2023 has been characterized by higher global rates and a volatile environment. Indeed, despite the potential last rate hike from the European Central Bank (ECB) and a pause from the Federal Reserve (Fed), the hawkish speeches from central bankers pushed the 10-year Treasury from around 3.84% to over 4.57%, and the German 10-year from around 2.39% to over 2.84%, reaching the highest levels of the year. Indeed, energy, which was one of the main sources of disinflation, is therefore set to become a positive contributor to price rises again by the end of the year, following the decision by the OPEP (mainly driven by Russia and Saudi Arabia) to extend their production cuts. This will penalize household purchasing power, but will also slow inflation's return to the central banks' targets.

Germany and US 10-year rates evolution

Sources: Carmignac, Bloomberg, 30/09/2023

In terms of local rates, we continue to see rate cuts in the emerging market (EM) universe this quarter with notably Poland cutting by 75 basis points from 6.75% to 6%, surprising the market. The majority of Latin American countries have already begun to lower their rates, but they are doing so cautiously, as they are no longer in line with the Fed's policy of "higher rates for a longer period". In China, the disappointing reopening continues to linger. The country is faced with a more difficult international environment due to the desire of many nations to regain industrial sovereignty and the United States to hinder Chinese development. Investors grew more pessimistic about the country’s economic outlook.

GBI-EM Index (Local sovereign debt index) - Yield Evolution

Sources: Carmignac, Bloomberg, 30/09/2023

Furthermore on FX, EM currencies continued to attract investors. Commodity exporter currencies and high carry currencies like those in Latin America remained appealing. Nevertheless, a selective approach is still required, keeping an eye out for balance of payments and inflation trajectories. As an example, the CLP has experienced a decline for three consecutive months due to the challenges encountered by the Banco Central de Chile in maintaining stable interest rates, particularly in light of the rapid decline in inflation within the Chilean economy.

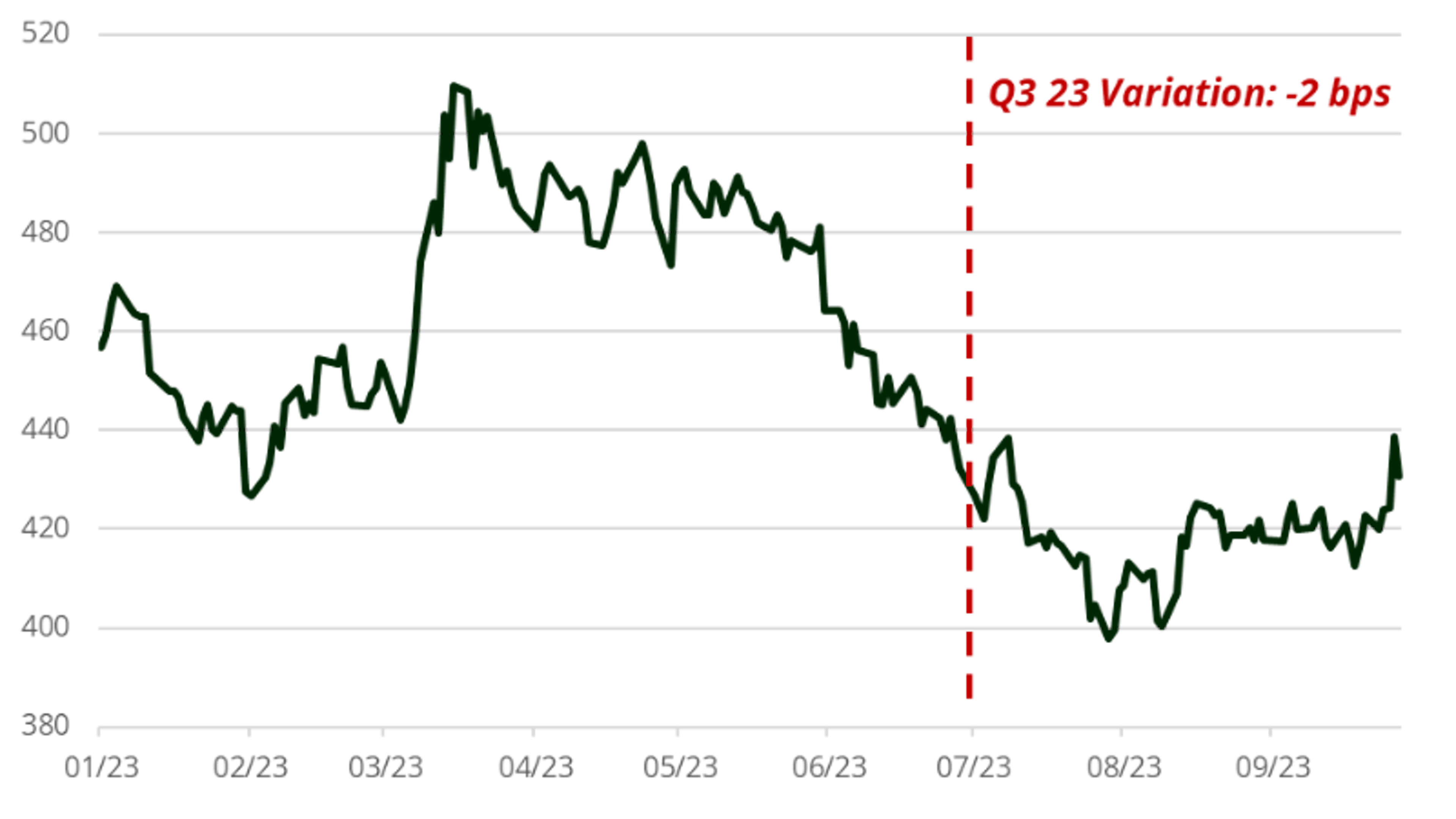

On sovereign credit, spreads remained stable over the period. Spreads were very tight in both the IG and HY spaces (distress names excluded) and the market kept a close eye on special situations such as in African countries. The sweet spot of this area remains in the BBs in which you can find the most attractive risk/reward opportunities.

J.P Morgan EMBIG diversified hedged EURO index (External sovereign debt index) - Spread

Sources: Carmignac, Bloomberg, 30/09/2023

What have we done in this context?

In this context we have mainly been impacted by our exposure to Local Rates in CZK, HUF, COP, MXN and CLP curves. The rise in US interest rates and the dollar, combined with the Chinese slowdown and rising inflation, have prompted us to reduce the risk in the portfolio. We notably reduced our exposure to the EMEA region, where valuations are not attractive as they were.

In the FX space we continue to enjoy the carry of EM FX currencies over the quarter. Nevertheless, on a risk management basis, we reduced our exposure to EM currencies and we continue to be selective and active in this segment. As an example, during the quarter we notably reduced our CZK exposure, which is directly impacted by oil imports. Following volatility peaks and increased in DM rates, we also increased our EUR exposure over the quarter.

On sovereign credit, we benefited from our exposure to the EMEA region, in particular through Romania. Lastly, over the period we increased on a tactical basis our exposure to Colombia as the country should benefit from the current trend on oil.

Outlook for the next months

Our view of recession and high rates is reflected in our portfolio construction, namely a large reduction of risky assets and a high level of CDS protections. We remain focused on duration with the view that a recession would force DM central banks to cut rates and thus enable further cuts in the EM world.

In Local Rates, we are closely monitoring EM Central banks to pursue their cutting cycles as the FED and ECB seem to have paused. We are ready to re-engage in countries which were among the most advanced in their rate hike cycle and in commodity exporters such as Colombia.

In Sovereign Credit, we continue to favour manufacturing countries that will benefit in the long term from the “nearshoring” phenomenon, i.e. the potential repatriation of production chains to closer and more stable countries (Romania, Poland, Mexico, etc.). Nevertheless, we remain cautious with protection against our HY names and will keep our positioning light and focused on the IG space.

Lastly, although we have reduced our global exposure to EM FX, we continue to favour a selection of currencies on a tactical/opportunist basis mainly in LATAM such as the Brazilian real and the Mexican peso.

Carmignac Portfolio EM Debt

Exploit fixed income opportunities across the entire emerging universeDiscover the fund pageCarmignac Portfolio EM Debt FW EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 5/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **

Main risks of the fund

Fees

- Maximum subscription fees paid to distributors

- 0,00%

- Redemption Fees

- 0,00%

- Conversion Fee

-

- Ongoing Charges

- 1.05%

- Management Fees

- 0,85% MAX

- Performance Fees

-

Footnote

Performance

| Carmignac Portfolio EM Debt | 1.1 | -10.0 | 28.9 | 10.5 | 3.9 | -9.0 | 15.3 |

| Reference Indicator | 0.4 | -1.5 | 15.6 | -5.8 | -1.8 | -5.9 | 8.9 |

| Carmignac Portfolio EM Debt | + 1.2 % | + 6.9 % | + 5.2 % |

| Reference Indicator | + 0.4 % | + 0.1 % | + 1.2 % |

Source: Carmignac at 28 Jun 2024.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor).

Related articles

Carmignac appoints UK Business Development Director

Emerging markets: looking at Eastern Europe

Carmignac Portfolio Flexible Bond in 3 minutes

Marketing communication. Please refer to the KID/KIID, prospectus of the fund before making any final investment decisions. This document is intended for professional clients.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. The information contained in this material may be partial information and may be modified without prior notice. They are expressed as of the date of writing and are derived from proprietary and non-proprietary sources deemed by Carmignac to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Carmignac, its officers, employees or agents.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. The reference to a ranking or prize, is no guarantee of the future results of the UCIS or the manager.

Morningstar Rating™ : © Morningstar, Inc. All Rights Reserved. The information contained herein: is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Access to the Funds may be subject to restrictions regarding certain persons or countries. This material is not directed to any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the material or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not access this material. Taxation depends on the situation of the individual. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA.

The risks, fees and ongoing charges are described in the KID (Key Information Document). The KID must be made available to the subscriber prior to subscription. The subscriber must read the KID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Funds present a risk of loss of capital.

The Funds’ prospectus, KIDs, NAVs and annual reports are available at www.carmignac.com, or upon request to the Management Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The French investment funds (fonds communs de placement or FCP) are common funds in contractual form conforming to the UCITS or AIFM Directive under French law.

In France, Luxembourg, Sweden: The risks, fees and ongoing charges are described in the KID (Key Information Document). The KID must be made available to the subscriber prior to subscription. The subscriber must read the KID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Funds present a risk of loss of capital. The Funds’ prospectus, KIDs, NAV and annual reports are available at www.carmignac.com, or upon request to the Management.

In the United Kingdom: the Funds’ respective prospectuses, KIIDs and annual reports are available at www.carmignac.co.uk, or upon request to the Management Company, or for the French Funds, at the offices of the Facilities Agent at BNP PARIBAS SECURITIES SERVICES, operating through its branch in London: 55 Moorgate, London EC2R. This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd. FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the FCA with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, Essex, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

In Switzerland: the prospectus, KIDs and annual report are available at www.carmignac.ch, or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, Nyon Branch / Switzerland, Route de Signy 35, 1260 Nyon.

The Management Company can cease promotion in your country anytime.

Investors have access to a summary of their rights in English on the following links: UK ; Switzerland ; France ; Luxembourg ; Sweden.