Flash Note

Carmignac’s model portfolio service: 1 year anniversary

What a year!

2022 will be remembered in multiple ways, but for us “financers” it will likely go down as one for the history books. It was the worst year for fixed income on record, in the wake of the most coordinated and fastest tightening cycle of all time along with the tug of war between inflation and growth concerns and the corollary sell-off across “secure” and risk-assets alike.

What a year to launch a new strategy!

The above led to one of the worst years for balanced and diversified funds as the sell-off affected both fixed income and equity markets in tandem, with few areas to hide to weather the storm. Challenging times indeed and one may argue that 2022 was the worst possible time to launch model portfolio solutions. While we can have some sympathy for such consideration, we would tend to argue that it has in fact been a great live test to appreciate the behaviour of risk-controlled model portfolios in such an extreme environment and demonstrate the virtue of an actively managed solution.

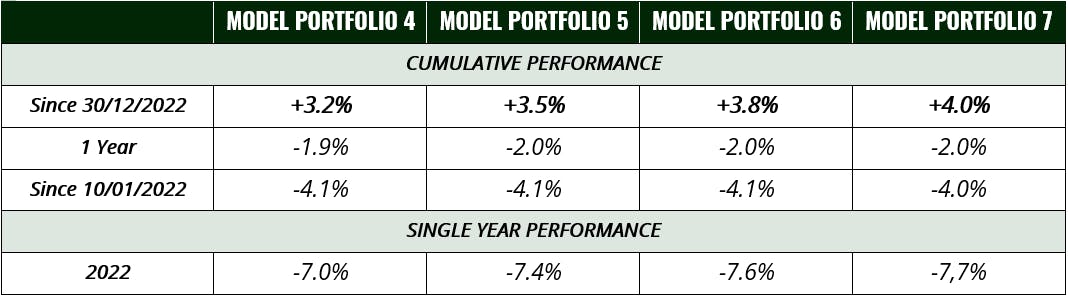

And by the looks of it, while returns are clearly below our long-term expectations, all of the portfolios have outperformed their composite benchmarks and are rapidly catching up from their lows.

These are good omens for the future.

Meanwhile on the risk front, all profiles remain largely in check with risk assessments.

Source : Carmignac, RSMR, 31/03/2023.

What can be expected going forward?

Diversification should be among the guiding principles for investors in 2023, even more so as the typical recession playbook may not apply the way it used to. While the global economy is expected to slow this year, the desynchronisation in both the economic cycles and the monetary cycles, the different main regional blocs are expected to dominate. Indeed, the coming months are expected to see a reopening boom in China, a slow recovery in Europe after the energy shock, and the United States entering a recession in the second half of the year. The disinflation trend will support economies and markets at the start of the year, but central banks should remain very vigilant on the inflation front.

In light of the above, we deem the following investment themes should prevail:

There is finally an alternative. After the worst year for fixed income markets in decades, the increase in global yields to levels not seen for a long time has made fixed income assets an attractive alternative to other asset classes which had taken the forefront in an environment of financial repression which has prevailed for the past 10 years or so. Despite valuations being slightly less attractive than a couple of months ago, the asset class should be an important performance driver in 2023.

Emerging market debt also offers compelling opportunities, notably in Latin America and Eastern Europe; countries that have hiked the most and are showing signs of “hike-fatigue” and inflation rolling over (mainly Brazil, Poland, Czech, Hungary) will be the most willing to change the policy messaging from a hawkish to a dovish tilt.

China has pivoted on 4 of the 5 risk factors which have been significant headwinds to the local and global economy. The shift in stance on the regulatory front allows for more attractive prospects in large technology groups. On the real estate front, we have seen the easing on both household property access and deleveraging targets supporting the sector, but also copper for which China accounts for 40% of global demand. And finally, the long-awaited reopening of China after 3 years of drastic mobility restriction has numerous implications. Most notably on consumption with more than USD 2.5 trillion of excess savings (i.e. equivalent to the GDP of France) to unleash benefiting both Chinese companies but also Western ones notably in high end consumer names.

Europe is recovering: having faced a “perfect” storm for most of 2022, the old continent is set to benefit from an improving growth outlook and renewed attractiveness for global investors which have been under-invested in the region. Consumer and business sentiment are set to be better oriented, with fiscal support and falling inflation as wages accelerate, supporting consumption. External demand is improving due to the US recession being deferred and the earlier than expected reopening of the Chinese economy. Furthermore, the replenishing of gas stocks lifts the overhang of rationing risk and pressure on the industrial sector in the second half of the year. Persistence in core inflation, a likely source of preoccupation for the Governing Council, will see the European Central Bank sticking to its tightening path. In addition, there is improving growth momentum, a strong tailwind for the Euro.

After this challenging year we will endeavour to reclaim the ground conceded in 2022, and demonstrate that the return of the business cycle, the end of financial repression and the desynchronisation of economic blocs around the world provide for fertile ground for active managers like Carmignac. Indeed, when the economic cycle is alive and (potentially) kicking, as an active manager you can anticipate when growth or inflation will roll over and position your portfolio accordingly. This is the essence of what we do.