Flash Note

Is 2023 the year to add China to your core allocation?

- Published

-

Length

4 minute(s) read

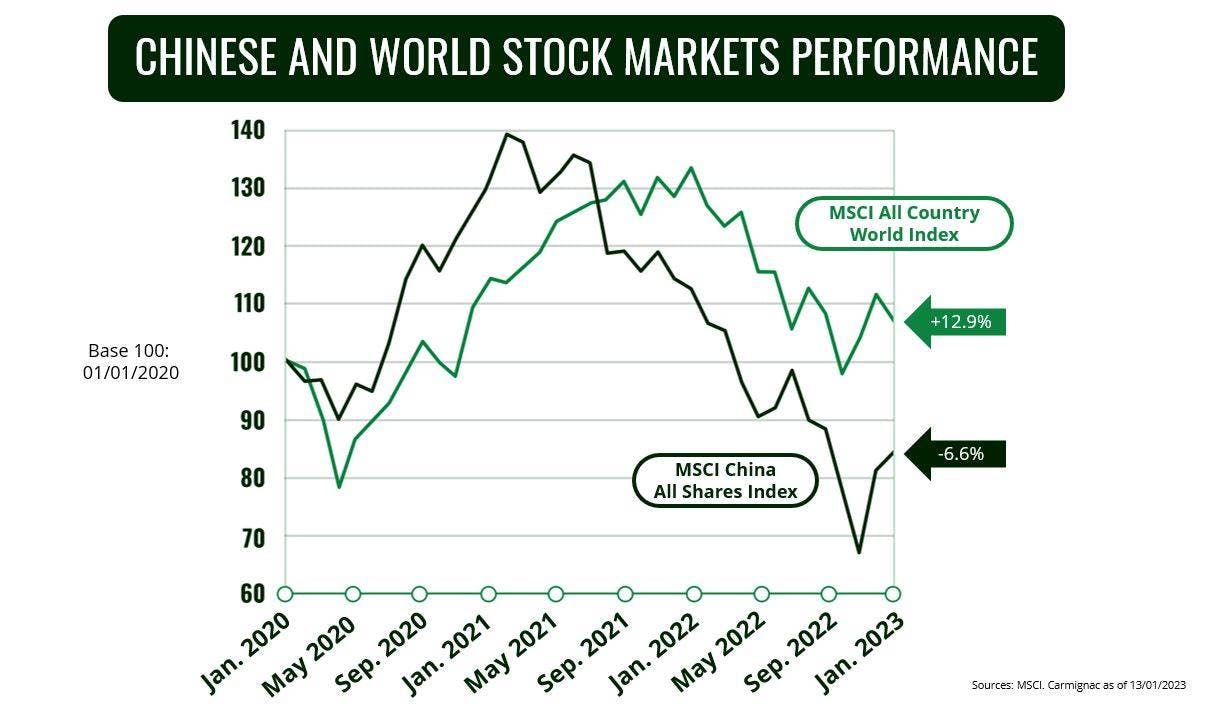

After nearly two difficult years for Chinese equities due to a regulatory crackdown, geopolitical tensions, and an economic slowdown, 2023 is looking more promising for investors.

China's financial markets experienced high volatility recently as several policy decisions and other developments fuelled foreign investors’ anxiety. These developments included tighter regulations for certain industries, the financial woes of real-estate giant Evergrande, and stricter transparency requirements for Chinese companies listed in the US. Not to mention Beijing’s strict zero-Covid policy and fears that China would invade Taiwan in the wake of Russia's invasion of Ukraine.

However, 2023 – the Year of the Water Rabbit, a symbol of peace, prosperity, a return to normal, and more – could open up a new chapter for investors. Recent crucial changes in the country point to a normalisation of its economy and financial markets and could usher in plenty of opportunities, particularly in consumer-oriented sectors.

A brighter future

Lights are flashing green again for Chinese equities. Of the five risk factors that weighed on Chinese stocks in 2021 and 2022 - tighter regulatory scrutiny, real estate crisis, zero-Covid policy, local politics and Sino-American tensions -, four have largely disappeared now that Beijing has finished tightening regulations and is even showing support for businesses, including internet heavyweights and property developers. The outlook for the fifth risk factor – US-China tensions which have jumped back after “Chinese Spy Balloon” incident would not see escalation in our view. We see economic recovery post-covid much powerful driver of Chinese equities in 2023.

The Chinese government has made concrete changes since the Communist Party Congress in October. The most significant one was lifting its strict zero-Covid policy – a necessary move that led to the reopening of the country (albeit somewhat abruptly) on 8 January. The government is also orienting its policy towards economic growth; at the China Economic Work Congress (the country’s biggest economic gathering), for example, leading policymakers announced that boosting domestic demand would be a priority in 2023.

The speed with which China is reopening its economy may cause some short-term difficulties, but we now expect GDP growth to pick up starting in the first half and reach around 5.0% for the full year. This would make China the only major economy whose GDP growth is accelerating.

Sanguine growth prospects fuelled by domestic demand

These factors point to a sustained increase in Chinese consumer spending, which should drive revenue growth for Chinese companies in consumer-oriented sectors for years to come. An upturn in Covid infections will likely weigh on consumer spending in the first quarter, but things are expected to improve as soon as Q2 as Beijing implements its pro-growth and pro-consumption measures and both city governments and households learn to deal more effectively with Covid-19.

What’s more, Chinese households are now sitting on excess savings of nearly 18 trillion renminbi (2.5 trillion euros), including 4 trillion renminbi accumulated since 2020 due mainly to the pandemic lockdowns. This should prompt an upswing in consumer spending. A job market recovery is also on the cards: nearly one in five jobs in China is Covid-sensitive because it involves physical contact, which means that the lifting of the zero-Covid policy and the full reopening of China’s economy are likely to stimulate both corporate hiring and consumer spending. This should underpin a rebound in household consumption.

Other structural growth drivers for domestic demand in China include: a 1.4 billion-strong population; a per-capita GDP of over USD 12,500; a rising household consumption rate; and a five-fold increase in total household consumption between 2005 and 2020. In addition, if we look at household consumption as a percent of GDP, it is now 54.3% in China – substantially lower than in developed countries (82.6% in the US, for example),1 indicating there’s considerable scope for Chinese consumer spending to expand further.

Other reasons to consider Chinese equities

There are many other reasons to invest in China. It has more than 6,000 listed companies with a combined market capitalisation of over USD 19 trillion,2 second only to the US, meaning it’s a stock market that simply cannot be overlooked by investors today. Yet despite the market’s size and momentum, Chinese companies make up only around 3.6% of the MSCI All Country World Index (which comprises stocks from some 50 countries), compared to 60.4% for US companies and 5.6% for Japanese ones.

Chinese companies are priced attractively. Their average price-to-earnings (P/E) ratio – an indicator of what investors are willing to pay for a company’s stock today based on its future earnings – is now around 113, slightly below its 10-year average, while global stocks are trading at a P/E ratio of around 15. In addition, most Chinese companies have cut costs over the past three years so revenue growth should drive an earnings recovery in 2023.

Finally, Chinese equities can provide effective portfolio diversification in terms of both geographic exposure and investment themes. We see particularly strong potential in four key areas of China’s new economy: 1) industrial and technological innovation, 2) healthcare, 3) ecological transition, and 4) consumption upgrade.

After 20 difficult months, 2023 could mark a new beginning for Chinese financial markets. Although there are some risks worth keeping an eye on (like an upswing in Covid infections and geopolitical developments), we believe many of them can be mitigated through active portfolio management. An agile, selective investment approach backed by a long-term vision – in keeping with the Year of the Water Rabbit – is what’s called for in 2023.

1Source: World Bank

2Sources : Bloomberg, CICC Research, 2022

3 P/E ratio for companies in the MSCI China Index, which comprises large and mid-cap companies listed on the Shanghai and Shenzhen stock exchanges.